Pricing a callable bond option

In this section, we will take a look at pricing a callable bond. We assume that the bond to be priced is a zero-coupon paying bond with an embedded European call option. The price of a callable bond can be thought of as:

Pricing a zero-coupon bond by the Vasicek model

The value of a zero-coupon bond with a par value of 1 at time  and prevailing interest rate

and prevailing interest rate  is defined as:

is defined as:

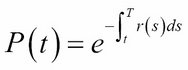

Since the interest rate is always changing, we will rewrite the zero-coupon bond as:

Now, the interest rate is a stochastic process that accounts for the price of the bond from time t to T, where T is the time to maturity of the zero-coupon bond.

To model the interest rate we can use one of the short rate models as discussed in this chapter as a stochastic process. For this purpose, we will use the Vasicek model to model the short rate process.

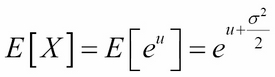

The expectation of a log-normally distributed variable  is given by:

is given by:

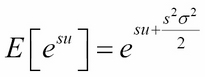

Taking moments of the log-normally distributed variable X:

We obtained the expected...